Collection of Canada mexico tax treaty ~ Nonresidents with permanent establishment in Mexico. Canada - Mexico.

as we know it recently has been searched by consumers around us, perhaps one of you. Individuals now are accustomed to using the internet in gadgets to view image and video data for inspiration, and according to the name of the post I will talk about about Canada Mexico Tax Treaty Amounts subject to withholding tax under chapter 3 generally fixed and determinable annual or periodic income may be exempt by reason of a treaty or subject to a reduced rate of tax.

Canada mexico tax treaty

Collection of Canada mexico tax treaty ~ Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006.

International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada.

The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. Canada has tax treaties like this with many countries around the world to. Canada has tax treaties like this with many countries around the world to. Canada has tax treaties like this with many countries around the world to. Canada has tax treaties like this with many countries around the world to. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income.

Income taxes on certain income profit or gain from sources within the United States. Income taxes on certain income profit or gain from sources within the United States. Income taxes on certain income profit or gain from sources within the United States. Income taxes on certain income profit or gain from sources within the United States. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties.

The existing taxes to which this Convention shall apply are. The existing taxes to which this Convention shall apply are. The existing taxes to which this Convention shall apply are. The existing taxes to which this Convention shall apply are. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not.

This Convention applies to income taxes imposed by each of the Contracting States. This Convention applies to income taxes imposed by each of the Contracting States. This Convention applies to income taxes imposed by each of the Contracting States. This Convention applies to income taxes imposed by each of the Contracting States. The MLI modifies Canadas tax treaties that are covered by the MLI. The MLI modifies Canadas tax treaties that are covered by the MLI. The MLI modifies Canadas tax treaties that are covered by the MLI. The MLI modifies Canadas tax treaties that are covered by the MLI. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990.

The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. The individual may credit the foreign income tax paid against the Mexican income tax liability. The individual may credit the foreign income tax paid against the Mexican income tax liability. The individual may credit the foreign income tax paid against the Mexican income tax liability. The individual may credit the foreign income tax paid against the Mexican income tax liability.

Certain exceptions modify the tax withholding rates shown in the table. Certain exceptions modify the tax withholding rates shown in the table. Certain exceptions modify the tax withholding rates shown in the table. Certain exceptions modify the tax withholding rates shown in the table. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force.

There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. Treaty Document. Treaty Document. Treaty Document. Treaty Document. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries.

A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada.

The complete texts of the following tax treaty documents are available in Adobe PDF format. The complete texts of the following tax treaty documents are available in Adobe PDF format. The complete texts of the following tax treaty documents are available in Adobe PDF format. The complete texts of the following tax treaty documents are available in Adobe PDF format. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. Canada listed its tax treaties with 84 countries for the purposes of the MLI. Canada listed its tax treaties with 84 countries for the purposes of the MLI. Canada listed its tax treaties with 84 countries for the purposes of the MLI. Canada listed its tax treaties with 84 countries for the purposes of the MLI.

Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. 2006 Income Tax Convention and Final Protocol French Text September 12 2006. 2006 Income Tax Convention and Final Protocol French Text September 12 2006. 2006 Income Tax Convention and Final Protocol French Text September 12 2006. 2006 Income Tax Convention and Final Protocol French Text September 12 2006.

For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page.

Pdf Multinational Firm Tax Avoidance And Tax Policy

Source Image @ www.researchgate.net

Canada mexico tax treaty | Pdf Multinational Firm Tax Avoidance And Tax Policy

Collection of Canada mexico tax treaty ~ Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. Diplomatic notes exchanged regarding the September 21 2007 signing of the protocol to the US-Canada income tax. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. 2006 Income Tax Convention and Final Protocol September 12 2006 Canada - Mexico. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006. Mexico and Canada signed a new income tax treaty and protocol on 12 September 2006.

International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. International tax treaty rates 1 1 This table provides general information and should not replace a careful review of any particular treaty. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. The Canada-Mexico Income Tax Convention was first signed in 1991 and updated in 2006. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada. Most of those countries are expected to become parties to the MLI and to list their tax treaty with Canada.

The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. The main purposes of tax treaties are to avoid double taxation and to prevent tax evasion. Canada has tax treaties like this with many countries around the world to. Canada has tax treaties like this with many countries around the world to. Canada has tax treaties like this with many countries around the world to. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income. However the credit is limited to the lesser of i the amount of foreign tax paid with respect to foreign-source income that is taxable in Mexico and ii the amount of Mexican tax corresponding to that income.

Income taxes on certain income profit or gain from sources within the United States. Income taxes on certain income profit or gain from sources within the United States. Income taxes on certain income profit or gain from sources within the United States. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. The provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income signed at Ottawa on April 8 1991 as well as the provisions of the Convention between the Government of Canada and the Government of the United Mexican States for the Exchange of Information with respect to Taxes signed at Mexico. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties. Withholding tax rates noted are those applied by Canada on certain payments to residents of selected countries with which it has signed international tax treaties.

The existing taxes to which this Convention shall apply are. The existing taxes to which this Convention shall apply are. The existing taxes to which this Convention shall apply are. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. The tax rates applicable to tax residents are 30 corporate tax rate and can go up to 35 for individuals. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not. 96 rows The rate as prescribed in the DTT assumes that the beneficial owner does not.

This Convention applies to income taxes imposed by each of the Contracting States. This Convention applies to income taxes imposed by each of the Contracting States. This Convention applies to income taxes imposed by each of the Contracting States. The MLI modifies Canadas tax treaties that are covered by the MLI. The MLI modifies Canadas tax treaties that are covered by the MLI. The MLI modifies Canadas tax treaties that are covered by the MLI. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990. Once in force the new treaty will replace the current Mexico-Canada income tax treaty of 8 April 1991 and the exchange of tax information agreement of 16 March 1990.

The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. The new treaty applies to residents of the states and does not restrict benefits accorded under domestic law or under any other treaty between. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. CANADA-MEXICO INCOME TAX TREATY A bilateral income tax treaty has been in effect between Canada and Mexico since July 17 1992. The individual may credit the foreign income tax paid against the Mexican income tax liability. The individual may credit the foreign income tax paid against the Mexican income tax liability. The individual may credit the foreign income tax paid against the Mexican income tax liability.

Certain exceptions modify the tax withholding rates shown in the table. Certain exceptions modify the tax withholding rates shown in the table. Certain exceptions modify the tax withholding rates shown in the table. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. Define which taxes are covered and who is a resident and eligible to the benefits often reduce the amounts of tax to be withheld from interest. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force. A tax treaty is covered by the MLI if both Canada and its treaty partner have listed the treaty for purposes of the MLI and have brought the MLI into force.

There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. There shall be regarded as taxes on income all taxes imposed on total income or any part of income including tax on gains derived from the alienation of movable or immovable property. Treaty Document. Treaty Document. Treaty Document. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries. Canada has tax conventions or agreements -- commonly known as tax treaties -- with many countries.

A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. A Subject to the existing provisions of the law of Canada regarding the deduction from tax payable in Canada of tax paid in the territory outside Canada and to any subsequent modification of those provisions -- which shall not affect the general principle hereof -- and unless a greater deduction or relief is provided under the laws of Canada tax payable in Mexico on profits income or gains arising in Mexico shall be deducted from any Canadian tax. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. The United States has income tax treaties or conventions with a number of foreign countries under which residents but not always citizens of those countries are taxed at a reduced rate or are exempt from US. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada. Technical Note on the Protocol amending the Income Tax Convention between the United States and Canada.

The complete texts of the following tax treaty documents are available in Adobe PDF format. The complete texts of the following tax treaty documents are available in Adobe PDF format. The complete texts of the following tax treaty documents are available in Adobe PDF format. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. Canada listed its tax treaties with 84 countries for the purposes of the MLI. Canada listed its tax treaties with 84 countries for the purposes of the MLI. Canada listed its tax treaties with 84 countries for the purposes of the MLI.

Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. Like the US-Mexico Tax Treaty the Canada-Mexico Tax Treaty provides for avoidance of double taxation reduction of income taxes applied to foreign residents. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation. In addition no credit is allowed for foreign taxes imposed on income that is exempt from Mexican taxation.

If you re searching for Canada Mexico Tax Treaty you've come to the ideal location. We have 20 images about canada mexico tax treaty adding images, pictures, photos, wallpapers, and more. In these page, we additionally have number of graphics available. Such as png, jpg, animated gifs, pic art, symbol, blackandwhite, transparent, etc.

2

Source Image @

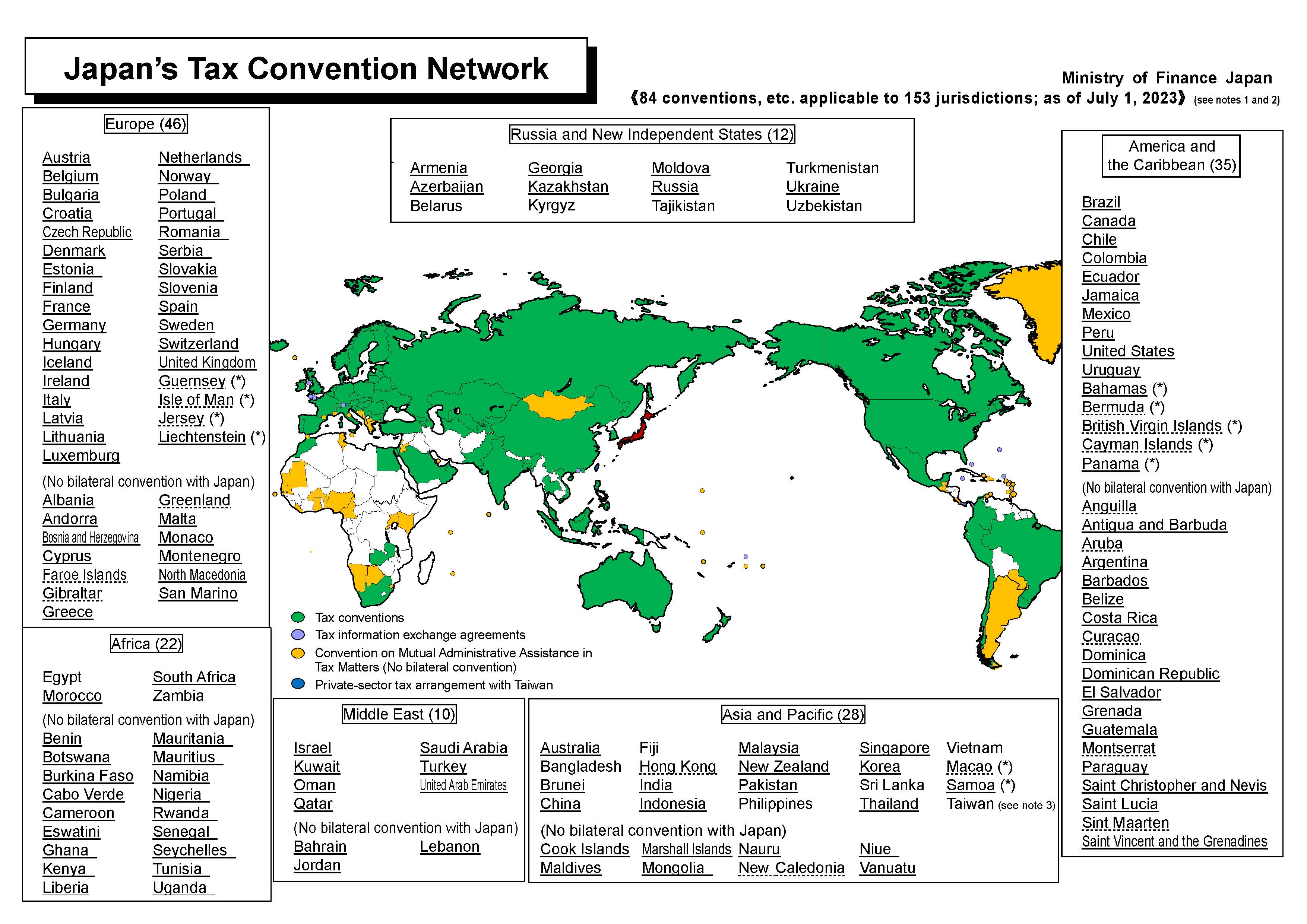

Japan S Tax Convention Network Ministry Of Finance

Source Image @ www.mof.go.jp

Pin On Living Abroad

Source Image @ www.pinterest.com

Us Expat Taxes For Americans Living In Mexico Bright Tax

Source Image @ brighttax.com

/cdn.vox-cdn.com/uploads/chorus_image/image/61626245/AP_18334483871272.1538522161.jpg)

/GettyImages-1081970868-692e94e35abf4c32a3d7c69cfc91ad75.jpg)